'Mortgage costs right now are terrifying'

Ian Thackray

Ian ThackraySearching for a new mortgage is time consuming when you have a demanding job, a new baby to care for and a Victorian home to renovate.

"Last time we looked properly, [the repayment] had pretty much doubled to £850 or £900 a month," says Ian Thackray. "It's terrifying quite honestly."

Ian's five-year fixed rate deal expires at the end of the year and the blacksmith and his partner, who is currently on maternity leave, find themselves, like so many others, in a "very difficult" situation.

They have been paying £450 a month for their terraced home in Blandford Forum, Dorset.

From August, when his partner returns to work, they need to factor in a monthly childcare bill of £600, and with Ian being self-employed, his wages fluctuate.

"There have been times on my way home from work when I've looked at the ads for Aldi, Lidl and Tesco and at £14 an hour, it's really tempting. If I have to give up being a blacksmith, then I will," the 39-year-old says.

The craftsman is not alone. Many are facing similar financial dilemmas as they contemplate rising mortgage costs.

The Bank of England has been steadily raising interest rates for the last year and a half, as it tries to tackle soaring prices.

After figures last week showed inflation not coming down as quickly as expected, many now predict the central bank will continue to raise rates from their current level of 4.5% to as high as 5.5%.

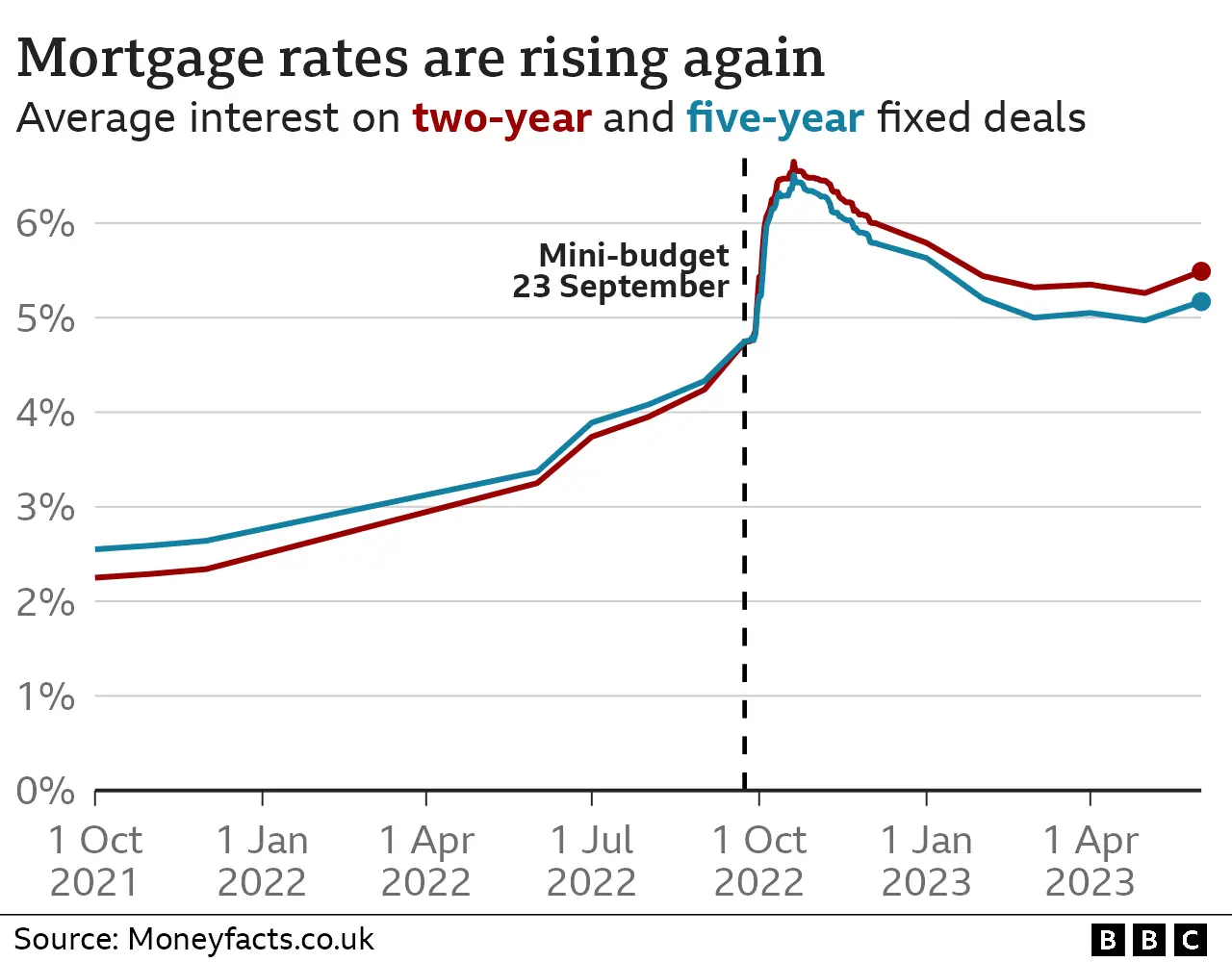

That in turn had an immediate impact on the mortgage market. Lenders began raising their rates. According to financial data firm Moneyfacts, the average two-year fixed-rate mortgage is now 5.49% and the average five-year fixed is currently 5.17%.

And within a week hundreds of mortgage deals were removed from the market as lenders reassessed their offers.

"Carnage" is how Craig Fish from Lodestone brokers in London described the situation.

"I'm currently on hold to NatWest - 30 minutes and counting - to discuss a possible new mortgage as they have just announced they are withdrawing rates at 10.30pm tonight. Do the lenders think the future is this uncertain?" he said earlier this week.

Jo Wilder

Jo WilderJo Wilder, 28, works for Cardiff Council and pays £700 a month for a studio apartment she has been renting for the past 18 months. She now wants to buy her own home - a process that is taking longer than she hopes, as she watches rates rise.

Despite having a healthy 20% deposit and a mortgage in principle, she says there are "not really any properties on the market".

Repayments on a three-year fixed-rate deal at 4.5% would be between £500 and £600 but she is worried about interest rates going up.

"It's not ideal. I'm just going to have to wait it out and hope rates come down. It really is very stressful," she says.

Jo had hoped getting her own place would mean a drop in monthly outgoings but with rising food prices she no longer thinks that will be the case.

"It is disheartening," she adds. "The way things are going I think it is actually going to be the same price, which is pretty daunting to be honest."

'A nightmare'

In Bedfordshire, Anthony Jones and his wife have a 14-month-old daughter - they want to upsize and have been trying to sell since last August.

The couple's five-year fixed deal has ended and they are now on a tracker mortgage, leaving them £200 worse off a month, at a little over £1,200.

"It's a bit of a nightmare," says Anthony. "We're looking at upsizing and all of a sudden are having to question the affordability of it."

The 33-year-old says when they first put their house on the market there had been "a lot of interest initially, then all of a sudden we had people saying 'our mortgage offer has been pulled' and 'we can't afford it anymore'."

The couple have reduced the asking price from £300,000 to £275,000, but say they cannot accept less because otherwise they will not have the deposit for their second home.

"Our daughter has grown so quickly, we need a garden and bigger bedrooms and more storage. The lack of space is even causing arguments between me and my partner," says Anthony.

What happens if I miss a mortgage payment?

- A shortfall equivalent to two or more months' repayments means you are officially in arrears

- Your lender must then treat you fairly by considering any requests about changing how you pay, perhaps with lower repayments for a short period

- Any arrangement you come to will be reflected on your credit file - affecting your ability to borrow money in the future

The upheaval for people going through the application process comes as Bank of England figures this week showed a decline in the number of mortgages being approved.

The number of net mortgage approvals for house purchases fell to 48,700 in April from 51,500 in March.

Mortgage broker London & Country is now seeing a trend for people fixing for one or two years, rather than the previous most popular five-year term, on the basis that interest rates will have fallen by the time they come to look for their next deal.

Spokesman David Hollingworth says people who are refinancing should start searching for a new product six months before the end of their current deal.

Some may want to consider taking out new mortgages over a longer term - something a lot of first-time buyers do to "give themselves breathing space", he says.

If it is a struggle to meet payments on an existing mortgage there is also the option of extending the term, but Mr Hollingworth says this is "not a move to be taken lightly because it will significantly increase the overall interest bill, by tens of thousands of pounds".

Are you struggling to get a mortgage or one that's affordable? Are you looking to re-mortgage following a fixed deal? You can share your experiences by emailing [email protected].

Please include a contact number if you are willing to speak to a BBC journalist. You can also get in touch in the following ways:

- WhatsApp: +44 7756 165803

- Tweet: @BBC_HaveYourSay

- Upload pictures or video

- Please read our terms & conditions and privacy policy

If you are reading this page and can't see the form you will need to visit the mobile version of the BBC website to submit your question or comment or you can email us at [email protected]. Please include your name, age and location with any submission.