When will interest rates go down again?

BBC

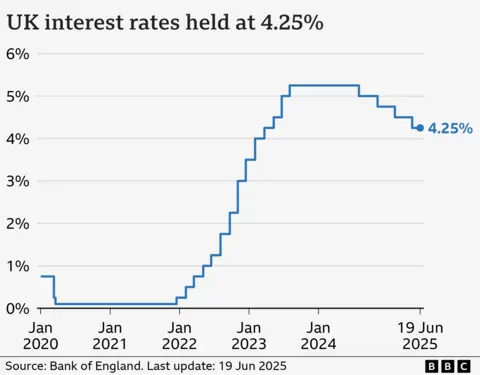

BBCThe Bank of England has held interest rates at 4.25% following two cuts earlier in the year.

Analysts expect the Bank's Monetary Policy Committee to announce further cuts later in 2025.

Interest rates affect mortgage, credit card and savings rates for millions of people.

What are interest rates and why do they change?

An interest rate tells you how much it costs to borrow money, or the reward for saving it.

The Bank of England's base rate is what it charges other banks and building societies to borrow money.

That influences what they charge their own customers for loans such as mortgages as well as the interest rate they pay on savings.

The Bank moves rates up and down in order to keep UK inflation - which is the increase in the price of something over time - at 2%.

When inflation is above that target, the Bank can decide to put rates up. This encourages people to spend less, reducing demand for goods and services and limiting price rises.

Once inflation is at or near the target, the Bank may hold rates, or cut them to stimulate spending and economic growth.

Will rates fall further?

It is difficult to predict exactly what will happen to interest rates, even in the medium-term.

The main inflation measure, CPI, was 3.4% in the 12 months to May 2025, the same as in the previous month.

Although that is far below the peak of 11.1% reached in October 2022, inflation remains above the 2% target.

As well as inflation, the Bank has to consider how the UK economy is doing more generally.

It also pays close attention to the performance of the global economy, which has been thrown into chaos by the widespread tariffs introduced by US President Donald Trump. Conflict in Israel and Iran has also created uncertainty.

Announcing its June decision to hold rates, the Bank hinted the next interest rate cut could come as soon as August.

Bank of England governor Andrew Bailey confirmed that "interest rates remain on a gradual downward path", although he warned that the world was still highly unpredictable.

Some analysts believe UK rates could fall to 3.5%.

How do interest rates affect mortgages, loans and savings rates?

Mortgages

Just under a third of households have a mortgage, according to the government's English Housing Survey.

About 600,000 homeowners have a mortgage that "tracks" the Bank of England's rate.

But the vast majority of mortgage customers have fixed-rate deals. While their monthly payments aren't immediately affected by a rate change, future deals are.

Mortgage rates are still much higher than they have been for much of the past decade.

As at 19 June, the average two-year fixed mortgage rate was 5.11%, according to financial information company Moneyfacts, and a five-year deal was 5.10%. The average two-year tracker was 4.91%.

This means many homebuyers and those remortgaging are having to pay a lot more than if they had borrowed the same amount a few years ago.

About 800,000 fixed-rate mortgages with an interest rate of 3% or below are expected to expire every year, on average, until the end of 2027. Their borrowing costs are expected to rise sharply.

You can see how your mortgage may be affected by future interest rate changes by using our calculator:

Credit cards and loans

Bank of England interest rates also influence the amount charged on credit cards, bank loans and car loans.

Lenders can decide to reduce their own interest rates if Bank cuts make borrowing costs cheaper.

However, this tends to happen very slowly.

Getty Images

Getty ImagesSavings

The Bank base rate also affects how much savers earn on their money.

A falling base rate is likely to mean a reduction in the returns offered to savers by banks and building societies.

The current average rate for an easy access savings account is 2.67%, according to Moneyfacts.

Any cut in rates could particularly affect those who rely on the interest from their savings to top up their income.

What is happening to interest rates in other countries?

In recent years, the UK has had one of the highest interest rates in the G7 - the group representing the world's seven largest so-called "advanced" economies.

In June 2024, the European Central Bank (ECB) started to cut its main interest rate for the eurozone from an all-time high of 4%. At its meeting in June 2025 the ECB cut rates by 0.25% to 2%.

In the US, the central bank - the Federal Reserve - cut rates three times in the latter part of 2024.

However the Fed has since held interest rates - most recently on 18 June. This means the bank's key lending rate's target range remains at 4.25% to 4.5%.

The Fed has repeatedly come under attack from President Trump, who wants to see further cuts.